|

"In the long term, it's hard for a stock to earn a much better return than the business which underlies it earns. If the business earns six percent on capital over forty years and you hold it for that forty years, you're not going make much different than a six percent return-even if you originally buy it at a discount. Conversely, if a business earns eighteen percent on capital over twenty or thirty years, even if you pay and expensive looking price, you'll end up with one hell of a result."

Charlie Munger

"Leaving the question of price aside, the best business to own is one that over an extended period can employ large amounts of incremental capital at very high rates of return."

Warren Buffett

Introduction

It's the time of year where forecasts and forward looking viewpoints about the economy, financial markets, companies and various industries, including the cannabis industry are put forth. The U.S. cannabis industry is similar and what we believe, read or know at this time about the U.S. cannabis market is:

1) Cannabis companies who participate in the regulated state markets in the U.S. will continue to invest significant amounts of capital in this capital intensive business as significant investment is required to build or buy dispensaries and cultivation/manufacturing/production facilities in support of sales growth. In addition to this, inflation is increasing development costs while deflation has simultaneously reduced flower prices.

2) Total revenue has grown significantly, state by state over the past three years and is expected to continue to do so based on organic growth in existing markets and further legalization in additional states in the U.S. Companies and analysts continue to focus on revenue and EBITDA growth in valuing cannabis companies.

3) Public companies posted strong period to period growth and y/y gains in revenue and adjusted EBITDA in calendar 2021 based on 1st, 2nd and 3rd quarter earnings releases.

4) Despite the strong increases in reported revenue and EBITDA, company stock prices and valuations have decreased steadily and significantly since their peak in early 2021 that was driven by the potential for positive U.S. legislation which does not appear to be imminent.

5) Forward looking public company revenue and EBITDA multiples are uneven looking across the industry as a whole as smaller companies are generally trading at lower multiples.

6) A view has emerged is that the industry will consolidate with smaller companies trading at lower valuations being bought out. History of consolidation in other industries suggests that consolidation will occur in the cannabis industry but I do not believe lower relative multiples between the buyer and seller will be the primary or only reason M&A deals get done.

7) The cost of debt capital has come down for the big four MSO operators who borrow at single digit rates, while smaller companies continue to borrow at significantly higher rates.

Public Cannabis Company Stock Prices and Valuation

Viridian Capital recently indicated valuations remain depressed in the cannabis industry owing to lack of meaningful catalyst to the upside tied to federal legislation, delays in major new markets, pricing pressure and execution on expansion as companies struggle with acquiring new assets and construction projects. As a result, cannabis industry forward valuations this year are significantly lower than last year at this time as follows:

2022 EV/sales 2.3x

2022 EV/EBITDA 8.0x

compared to:

2021 EV/sales 4.1x

2021 EV/EBITDA 16.4x

So what gives? Despite the issues, many cannabis companies have reported significant increases in y/y revenue and adjusted EBITDA in 2021 as the market has continued to grow. In connection with and beyond the issues mentioned above, this article will discuss how the cannabis industry should adopt and develop alternative/additional valuation metrics that provide additional insight into company value creation and drivers as well as better measure capital allocation performance in the industry.

I will start my discussion by stating that markets are forward looking and that valuations focused on revenue/EBITDA growth and related multiples are at best incomplete and at worst misleading owing to unique characteristics of the cannabis company financial model. This is due to the fact that EBITDA does not measure the impact of taxes on valuations which are significant in the cannabis industry due to 280E. EBITDA also does not directly address cap-ex requirements which are significant in the industry and will continue to be substantial in support of future revenue growth based existing turnover ratio relationships that exist across the industry as well as inflation of development costs.

In August 2021 Michael J. Mauboussin, a highly regarded and well known valuation expert at Morgan Stanley published a well received research report titled "Everything is a DCF Model" where he states that for investors valuing a stake in a cash-generating asset, they should recognize that they are using a discounted cash flow model. Mauboussin states that this is important because the value of businesses is the present value of the cash they can distribute to their owners. Mauboussin states that this topic deserves attention because many market participants now, as in the past, don't think that DCF models are relevant. In the cannabis industry most of the valuations I have seen in 2019 - 2021 were based on multiples of revenue and EBITDA and market multiples which means comparisons of these multiples between companies. The article went on the say that there are a number of explanations why DCF models are not used more consistently and properly by the private and public markets that include the following:

1) The public markets are pretty good at valuation so most investors defer to its ability to reflect what is out there and thereby turning their attention to whether results will be better or worse than the market's expectations.

2) Small changes in assumptions for a DCF model can lead to big changes in value. As a result, many investors are more comfortable using multiples of earnings or cash flow as proxies for valuation.

3) Lot's of valuation is done by comparison and there are two ways to come up with a value for a financial asset. The first is to calculate intrinsic value by discounting future cash flows. The second is to compare investments in the market.

4) Valuation is tricky early in a company's life cycle. Start-ups are difficult to value using a DCF model because the range of outcomes is wide.

5) It is hard to value early stage companies that are losing money.

Mauboussin goes on to say that each of these reasons explain why DCF models are not used more widely but indicates that these reasons do not stand up to scrutiny. I agree with Mauboussin when he says that even if you choose not to build a DCF model for the investments you make, it is still useful to keep in mind the factors that drive value which include; growth from investment that earn returns in excess of a company's cost of capital, competitive advantages of a company that will allow it to continue to earn excess returns on capital deployed as well as a company's TAM and market share.

For cannabis company valuations, my opinion is that DCF models that address the factors that drive ROIC, future cash flows, risks and discount rates are the best tool to depict what drives intrinsic company value. Since company equity value is driven by a company's return on invested capital (ROIC) and ROIC must be greater than a company's weighted average cost of capital (WACC) to create value, I compare historic and current ROIC/WACC spread performance relationships to the future ROIC/WACC spread performance relationship in DCF and economic profit models in total and on a projected per share basis.

My view of the equity market is that for the most part, it is rational. McKinsey states this well by saying in the 7th edition of Valuation that there is compelling evidence that valuation levels for individual companies and the stock market as a whole clearly reflect the underlying fundamental performance in terms of return on capital and growth. McKinsey states that , yes there are times when valuations deviate from fundamentals, but these typically do not last long. Evidence also shows that some widespread beliefs espoused by managers and finance professionals are inconsistent with fundamental principles of valuation and are erroneous. Belief in this is why I build models in attempt to better understand present and future potential company value.

Cannabis company equity valuation models based on multiples of revenue and EBITDA do not address significant cash flows related to 280E income tax costs and capital investment in the form of working capital and capital expenditures that have a significant impact on company valuations. ROIC and DCF models that are put together well, address these issues. Cannabis multiple comps that do not address ROIC, ROIIC and the duration of growth are for the most part, useless.

What we know is that high ROIC business generate more distributable cash per dollar of earnings than low ROIC businesses and are worth more and are therefore assigned higher valuations. One of the best explanations of this approach comes from Amazon's founder, Jeff Bezos in his letter to shareholders in Amazon's 2004 annual report and also discussed in a letter to investors by Ensemble Capital, an investment firm that focuses on company ROIC in its portfolio strategy and investment making decision process..

In Jeff Bezo's Amazon letter, Bezo's illustrates how a company with significant annual sales growth (100% y/y for several years) at 55% gross margins generates earnings and EBITDA that doubles each year at the same time the company generates significant negative free cash flow and return on investment due to significant cap ex requirements. Bezo's states that Amazon's ultimate financial measure and goal is to drive over the long-term, free cash flow per share. Please see the 2004 Amazon letter to shareholders for the detailed example. What is interesting about the Amazon financial model example is that it is comparable to the cannabis industry financial model in that sales and EBITDA have grown for companies in the cannabis business on a y/y basis while free cash flow has not, due to significant capital requirements for cap ex and working capital expenditures along with high effective tax rates associated with 280E.

I have built financial models on 18 public cannabis companies that include ROIC calculations for each company based on operating results by quarter for the quarters ending 9/30/21, 6/30/21, 3/31/21, 12/31/20 and 9/30/20, as well as for the years ending 12/31/17 - 12/31/20.

Based on aggregate data from my individual public company models and personal view, I built two hypothetical cannabis industry financial models that are less complex than typical actual models. They include the following assumptions:

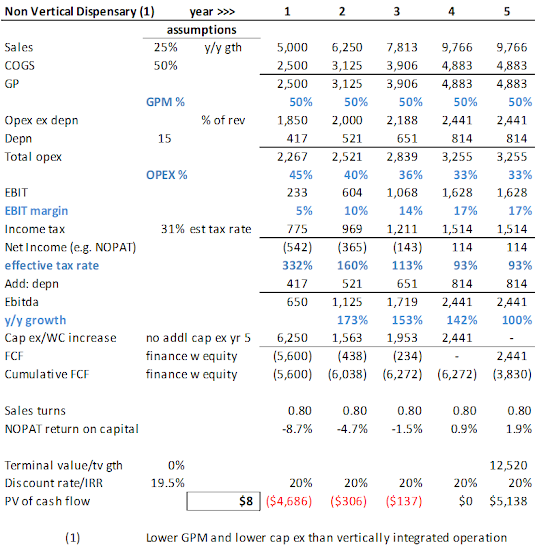

1) Significant y/y sales growth of 25% per year for four years before growth flattens out in year five.

2)Fifty percent and sixty percent gross margin assumptions in non vertically integrated and vertically integrated models, respectively.

3)EBIT margins that increase from 5% in year one to 22% in year five.

4) An estimated combined federal and state 280E tax rate of 31%.

5) Invested capital requirements for working capital and cap-ex based on comparable aggregate turnover rate of the eighteen public cannabis companies that I modeled.

6) The gross profit margin and cap ex is increased while FCF is significantly decreased for several years in the vertically integrated model compared to the non vertically integrated model due to investment in cultivation and production capacity resulting in a lower rate of return.

Hypothetical Industry Model Results

1) Both models include significant EBITDA growth on a y/y basis at growth rates greater than 100%.

2) Free cash flow is significantly negative in both models over the five year period depicted in the models despite the growth in revenue and EBITDA due to cap ex requirements, tax and actual industry turnover ratios.

3) No intrinsic value is created in years 1 - 4 despite significant revenue, margin and EBITDA growth in each year. All intrinsic value is created in year five in both models due to FCF, terminal value assumption and zero incremental capital investment requirement required due to zero top line sales growth.

4) The hypothetical company generates negative ROIC in years 1 - 3 with marginal but below WACC results in years 4 and 5.

5) The IRR in the models is lower in the vertically integrated model than the non vertically integrated model. All of the IRR is attributable to the year 5 terminal value as no value is created in years 1 - 4.

In summary, the sales growth, margins and EBITDA growth for the cannabis company are very positive but the models do not produce any real returns for sometime while they produce significant negative cash flow, per share or otherwise and negative ROIC's. Unfortunately, as the examples indicate, the businesses are fundamentally flawed. Jeff Bezo's would not be invested in these businesses. See Exhibits 1 and 2 below for the financial models.

Exhibit 1- Hypothetical Non Vertical Dispensary Financial Model

Exhibit 2- Hypothetical Vertically Integrated Dispensary and Cultivation Facility

Source: Gregg Carlson calculations and aggregated industry data

Actual ROIC for Public Companies in the U.S. Cannabis Industry

The list of metrics investors look at when analyzing businesses is long and typically includes revenue growth, operating margins, EBITDA and net income, among others. Cannabis businesses are no exception, with the focus for public companies being revenue growth, operating margins and EBITDA.

No financial metric is perfect and I believe that solely focusing on revenue growth and EBITDA is not effective at this stage of the cannabis industry development. ROIC is also not a perfect metric and is not currently widely used in the industry due to the industry's high growth land grab mode state of development that so far has led to subpar returns on capital. Like other high growth industries, the cannabis industry will eventually mature past its growth without ROIC strategy.

There is ample research that indicates growth and return on capital contribute to company value and it is well known that high returns on invested capital is more sustainable than high rates of growth. Investors care about the future cash generation of a business and cash is generated by expanding the business as well as by optimizing the amount of cash that must be invested in a business to achieve growth. It is not next year's results that matter or the one after that as value is ultimately determined by the sustainability of these metrics over many years instead of their outcome over one or two. McKinsey points out that revenue growth is not sustainable as growth rates tend to decay over several years. When growth decays, growth tends to decay at rapid rates. For firms with high ROIC, ROIC tends to decay at a much lower rate than sales growth decay. Putting this together means that the valuation premium for high ROIC companies is more persistent than the valuation premium associated with high growth rates.

The regulated cannabis industry has been in a period of high overall revenue growth and significant investment without producing ROIC in recent years and quarters. Equity investors have woken up to this fact and adjusted company stock prices and valuations accordingly as companies now stand on their own fundamentals without a near-term positive legislation catalyst.

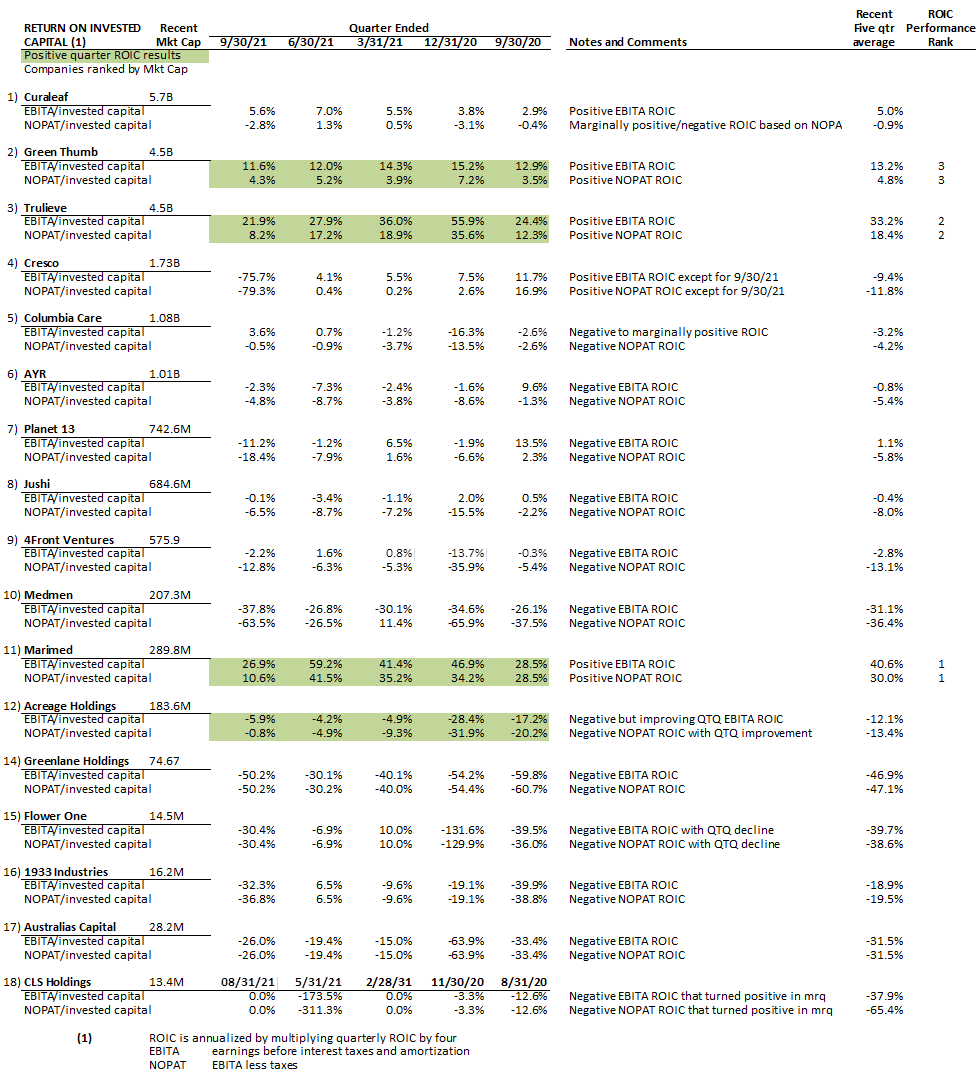

We calculated ROIC on 17 U.S. public cannabis companies from the largest market cap to small cap public cannabis companies for the last 5 quarters as of the quarter ending 9/30/2021 based on company public financial report filings. Our two ROIC calculations for each company were based on EBITA to invested capital and NOPAT to invested capital as defined below:

EBITA/Invested capital = ROIC

is defined as:

EBITA = Earnings before interest, taxes and amortization (i.e. depreciation is included here)

Invested capital = Total assets less current liabilities adjusted for current portion of long term debt and leases.

NOPAT /Invested capital = ROIC

is defined as:

NOPAT = EBITA minus taxes

Invested capital = same as above.

Please note that the ROIC difference between EBITA and NOPAT is significant for the cannabis industry due to 280E.

ROIC addresses how well companies deploy capital and create value for shareholders. The primary focus for cannabis industry investors was initially revenue growth, followed by EBITDA growth now followed by return on capital. The equity market now focuses both on the P&L and balance sheets of individual companies while a fair number of management teams remain focused on growth at the same time they consistently produce negative ROIC which is not a sustainable strategy. As the industry becomes more institutionalized, focus on TAM, TAM share, ROIC and future free cash flow will continue to increase.

I modeled eighteen U.S. public cannabis companies and out of eighteen, only three produce positive returns on invested capital. The big three ranked by ROIC performance are:

1) Marimed

2) Trulieve

3) Green Thumb

They are viewed as strong capital allocators and have generated significant positive ROIC's. Beyond these three companies, most of the remaining companies in the universe have produced negative returns on capital which is not sustainable, in my opinion. Between these extremes, two companies have shown some recent quarter to quarter improvement in ROIC. They are Acreage Holdings and CLSH Holdings, USA.

In fairness to current negative producers of ROIC, I must point out that it remains to be seen how their future plays out, as it will depend on their capital allocation/execution ability, ROIC, competitive factors and results that have yet to be written. The top three ranked companies have achieved significant credibility in terms how they have managed their financial models and allocate capital based on their results so far. Will wait to see if they can maintain the ROIC performance they have achieved so far. See below for my complete list of ROIC results based on EBITA and NOPAT.

The future will be interesting as we see how, when and if additional companies transition from being negative ROIC to positive ROIC producers which could result in higher valuations in my view. Beyond the transition to positive ROIC, companies will need to generate a positive spread over time between ROIC and WACC associated with their invested capital base in order to create shareholder value that is most effectively modeled, measured and managed using DCF and economic profit models. It remains to be seen if this can be accomplished in individual companies, even though overall industry sales are expected to increase for several more years. The model format for calculating a company valuation based on economic profit is:

Multiply:

invested capital by year x ROIC vs. WACC spread = Economic profit x discount rate = PV of econ profit

calculated by year during explicit forecast period

sum:

PV total of years forecast and add continuing value forecast

Adjust for cash debt and leases

Equals equity value.

See Exhibit 3 below for my company by company ROIC calculations.

Exhibit 3 - Public Cannabis Company Return on Invested Capital in Recent Quarters

Source: Gregg Carlson calculations based on company press releases and public financial filings

Industry Level ROIC and ROIC Deconstruction

We deconstructed ROIC for each company and for the industry as a whole, between revenue turns and EBITA/NOPAT margins. We also compared the top three performers to overall industry results as follows (see Exhibit 4 below).

Exhibit 4 - Deconstructed Cannabis Industry ROIC compared to Top Performers

Source: Gregg Carlson calculations based on company filings

The industry data shows that the industry achieved sales turns of approximately 49% during the last four quarters during a period when revenue increased overall on a combined basis for the 18 companies included in the calculation by approximately 65% y/y. While the industry experienced significant growth in revenue it achieved marginal to negative EBITA and NOPAT margins.

Summary

The top three ROIC performers achieved higher, comparable and lower y/y sales growth (146%, 64%, and 48%, respectively) than the industry average but achieved both higher turnover (i.e. dollars of sales per dollars of assets) and positive EBITA and NOPAT margins than the industry, thereby driving positive ROIC compared to a negative industry ROIC. During the period measured, almost all other industry participants achieved negative EBITA and NOPAT margins that more than offset sales turnover resulting in negative ROIC. The underperformers, are the majority of companies here. EBITA includes depreciation which is a real cost in the capital intensive cannabis industry MSO or MSO like financial model. NOPAT includes taxes which is also a significant cash flow cost due to 280E. For the companies that are delivering negative EBITA, NOPAT and ROIC, they will need to develop or tweak existing business models and possibly investment strategies so positive EBITA, NOPAT and positive ROIC WACC spreads are achieved or they risk going by the wayside despite delivering sales and adjusted EBITDA growth. Long-term investors put up cash today in hopes of positive cash on cash returns over a holding period measured in years. This happens when companies put capital to work that generates positive ROIC WACC spreads over time. In the cannabis industry, this has been difficult to do for the majority of the companies depicted here due to negative returns on invested capital and/or positive returns that are less than higher cost WACC.

Companies that can ultimately put capital to work at a high ROIC and positive spread can create a significant amount of equity value over time. So far , this has been difficult to do for all but a handful of operators in the cannabis industry. The jury is out as to whether the majority of the Cannabis companies discussed here can achieve this despite expected ongoing sales and adjusted EBITDA growth. Results will be driven by how well they execute their forward looking investment profile in terms of magnitude of growth and ROIC. The industry so far has taken an inside view with its focus on growth. The most successful cannabis companies will also take an outside view as they recognize that institutional investors who invest for the long-term are able to invest in any industry that can generate high rates of ROIC and positive ROIC/WACC spreads and may or may not avoid companies and industries that do not.

For additional readings and further discussion of corporate finance, DCF models, economic profit, ROIC , ROIIC and WACC please see the endnotes and further readings below.

Endnotes

[1] Jonathan DeCourcey, "Ten Predictions for US Cannabis in 2022, Viridian Capital Advisors, December 30, 2021.

[1] Michael J. Mauboussin and Dan Callahan, CFA, "Everything Is a DCF Model," Consilient Observer: Counterpoint Global Insights, August 3, 2021.

[1] TAM means total addressable market.

[1] Tim Koller, Marc Goedhart and David Wessels, Valuation: Measuring and Managing the Value of Companies, 7th Edition (Hoboken, NJ: John Wiley & Sons, 2020), 99 - 126.

[1] ROIC means return on invested capital while ROIIC means return on incremental invested capital.

[1] Jeff Bezos, Letter to Shareholders, Amazon 2004 annual report.

[1] Sean Stannard-Stockton, CFA,"Return on Invested Capital: Why It Matters & How We Calculate IT," Ensemble Capital, April 2016

[1] Tim Koller, Marc Goedhart and David Wessels, pages 171 - 172.

[1]Sean Stannard-Stockton, CFA, "The Sustainability of Growth vs. Return on Invested Capital," Ensemble Capital, September 21, 2016.

10 See Tim Koller, Marc Goedhart and David Wessels,

McKinsey & Company, Valuation 7th edition, page 104 for example of a

valuation using discounted economic profit.

For Further Reading

Gregg Carlson, "US Retail Industry Research, Costco Wholesale Corporation, The Beat Goes On," March 14, 2012.

The Scuttlebuttt Investor, December 17, 2016.

Michael Mauboussin and Dan Callahan, CFA, "Calculating Return on Invested Capital," Credit Suisse, June 4, 2014.

Michael Mauboussin and Dan Callahan, CFA, "Market-Expected Return on Investment," Morgan Stanley, Counterpoint Global Insights, April 14, 2021.

Bin Jiang and Tim Koller, " Data Focus: A Long -term look at ROIC," The McKinsey Quarterly, 2006 Number 1.

Disclosure and terms of use statement

The analysis and opinions expressed in this report reflect the personal view of the author. This report is not a solicitation to buy or sell securities. No part of the author’s compensation was directly or indirectly related to specific recommendations or views expressed in this research report. Readers should consider this report as only a single factor in making investment, business and/or economic decisions. As the author-we are not your advisor the author-we do not take responsibility for any action you take based on this report. This publication is provided to you for information purposes only. The views in this publication are those of the author and are subject to change, and the author has no obligation to update the opinion or information in this publication. The author does not accept liability for any direct or indirect losses arising from use of this publication or its contents. The author recommends that readers of this report consult with any personal advisor’s they deem necessary before taking any actions based on this report. Actual results may and are likely to be materially different than those indicated in this report. The author-we have received no compensation from the companies mentioned in this report in connection with this report and may or may not have an economic and/or advisory relationship with any companies mentioned in this report. The author may or may not own shares in any of the companies mentioned. The author does not provide tax or financial advice and nothing contained herein should be construed to be tax or financial advice. Please note that this report was originally prepared for and issued to approved market professionals, professional advisors and to specific client relationships. Recipients of this report who are not designated recipients should not use its contents, take action based on its contents and/or redistribute the report. This report should not be relied on as a substitute for the exercise of independent judgment. We believe the information and opinions included in the report are complete and accurate. Information and opinions included in the report were obtained from sources that we believe are reliable. We make no representation as to their accuracy or completeness. We accept no liability or loss arising from use of the material presented in this report. The information presented in this report is provided to you for information purposes only and is not considered as an offer or the solicitation to sell or to buy or subscribe to securities of other financial instruments. We will not treat report recipients as its customers by virtue of receiving this report. This report and its contents may not be altered, transmitted to, copied or distributed to any other party, without prior express written permission of the author. You may not reproduce, distribute, transmit, disseminate, sell, publish, display, broadcast, circulate or forward any part of this report to anyone, including but not limited to others in the same company or organization, without express written consent of the author. This requirement and limitation includes, for example, electronic activities such as emailing, scanning, web site posting, downloading, printing, photocopying, faxing and the like. Authorized recipients may print a single copy (not multiple copies) solely for your own personal use. No other copying of any kind is authorized

Transaction Close and Value is Influenced by State of Readiness

Gregg Carlson

Updated from 2019 post

7/01/2021

You are a business owner or CEO who has built up your private company over time and have made the decision to sell all or part of your business. You put your company on the market and hope to arrive at a favorable enterprise value figure with a purchaser. While your company may or may not have been audited or reviewed by a CPA firm, your ability to complete a transaction will be significantly influenced by this issue and your ability to complete the due diligence process.

Most of the sell side transactions I have been involved with, were private firms that had a history of being audited by an outside CPA firm. In cases where sellers have not been audited or reviewed, the batting average for completing a sell side transaction is lower based on my experience.

The reasons for having your private company audited or reviewed typically include:

2)

to eventually sell the business or take on a partner; and

3)

to issue debt or meet partnership agreement requirements, among other factors.

To complete an audit successfully, your accounting function will have to deliver prepared by client schedules (PBC's) before fieldwork begins, support audit fieldwork by answering questions and providing documentation, support internal control testing and review and be responsible for preparing financial statements and footnotes in a required format that is the basis for the CPA firm's audit opinion. In regard to PBC's, the PBC's will need to tie to the company general ledger-trial balance and basic financial statements (i.e. balance sheet, income statement, cash flow statement and footnotes where applicable), as well as be in a lead sheet and balance sheet roll-forward format. The company will typically designate a member of the financial team to be the liaison to the audit firm who has enough clout in the organization to influence the company's priorities to complete the project successfully (i.e. on time within a budget resulting in a clean opinion). In this day and age the audit process has become more complex due to the increased complexity of GAAP and other factors that result in a long complex deliverable list for the business being audited.

In addition to baseline requirements described here, sell side transaction itself adds to the burden and complexity of the audit process due to financial reporting and other requirements related to the sales transaction itself that must be adhered to by the seller or buyer or both.

If you are seller who has the ability to successfully complete the audit process in general or in connection with a transaction, your incremental overriding management issue will be managing the sell side transaction due diligence deliverable requirements and overall process within a typically tight stressful time line while simultaneously running the business day-to-day. Unless you have the necessary transaction related human resources and expertise, you will typically not have the ability to do both.

Sell side transactions I have worked on typically begin with information that is provided to the general marketplace of prospective buyers within an industry. The buyer list is then narrowed down to a smaller list of prospective buyers where additional information is provided followed by identification and agreement with a single buyer. At the initial stage until a purchase agreement is signed off key factors and disclosures in the due diligence process may include:

1) Is the seller selling assets or stock? The answer to this question directly affects the seller's after tax returns on the sale. This is a seller decision that may or may or may not be negotiated with the buyer;

2)

defining and calculating net working capital;

3)

analyzing key metrics such as sales trends-key markets & customers, margins

and other key performance metrics;

4)

defining and calculating free cash flow, earnings and/or Ebitda on a trailing

twelve month basis or other historic time period as a basis for the valuation;

and;

5)

Other factors depending upon the nature and specifics of the transaction including,

industry trends, Comps-benchmarks, KPI's, key competitors and technology

issues, for example.

At this stage, the transaction process has just begun. At some point in the process the buyer is identified and a purchase agreement is entered into that must be adhered to in order to get to the transaction close. What follows are typically a list of due diligence requests and requirements that put further stress on the accounting function of the seller, some of which may or may not precede the transaction milestone of reaching a purchase agreement. In general a significant list of buyer requests that are uploaded to a data room after the purchase agreement has been reached typically include the following;

1) Additional detailed financial information that includes current and historical internal financial statements and analysis specific to the company or industry or both;

2)

audited financial statements, where available;

3)

internal budget, budget to actual and forecast data;

4)

stub period financial information;

5)

trailing 12 month, 24 month, 36 month or longer financial history;

6)

trends in revenues, costs and margins;

7)

information about key products, customers, markets and customer churn + value information;

8)

key contracts and agreements;

9)

litigation and legal matters;

10)

ownership and debt issue related information;

11)

environmental and technology issues, where applicable;

12)

labor force information;

13)

new business and market information;

14)

requests for unique, customized and specific information not normally produced

by the seller;

15)

detailed information about specific assets and liabilities, and;

16)

other and ad hoc information as well as a long list of deliverables that are

unique to the transaction and much longer and more specific than this summary.

It is safe to say that the process will likely be a stressful experience that demands specialized transaction and project management experience. It will also produce a significant workload in a compressed timeframe. The accounting function of the seller will bear a significant burden in support of the transaction. Accounting departments that are often viewed as overhead and less important to a business become a high priority in the transaction, which can be problematic if their importance is not recognized, prioritized and supported by the business during the transaction.

Successful transactions I have participated in, were sales of companies that typically had a history of external audits performed by a credible CPA firm. In some cases this was mandated by industry regulations or financial stakeholders (equity and/or debt holders). In other cases, the company themselves undertook this exercise voluntarily. No matter what the original reason was, when it came time to sell, the external audit, even if not a requirement, was a significant factor in the sale transaction.

While not a rule of thumb, potential sales of entire businesses or specific assets within a business I witnessed that had not been audited or reviewed in several cases did not make it through the due diligence process. There are a number of reasons for this, but the primary factor is overall seller credibility and the fact that financial information included in financial statements and/or internal controls could not be relied on by the buyer without a significant amount of work being done at a large cost. Given that companies typically sell at a multiple of earnings, cash flows or revenues, an investment in an external audit or review typically more than pays for itself. Having said this, getting through the due diligence process of a sales transaction takes more than completing an external audit or review.

Furthermore, even with the completion of years of audits, the transaction itself typically adds additional burden to the seller as described herein and influences the audit itself due to the risks associated and financial reporting requirements specific to the transaction, among other factors.

For example, let's say your company has been audited and is being asked to provided comparative financial statements by the buyer in a situation where revenues, costs and expenses have been reclassified from year-to-year due to changes in the business or financial reporting processes or transaction types. In this case the buyer will ask that your current year numbers be classified consistently with prior year numbers. If you have not kept your books in this manner in the current year, this can be a problem that may be expensive to fix and one that could slow down the completion of the current year audit which in turn could slow down the close of the company sale transaction.

In situations where the seller that has been audited in prior years is selling to a public company, where public company reporting requirements mandate that the private company report on stub periods, and requested prior year comparative periods that do not match the historic year end reporting periods of the seller as well as variations on these themes, the seller may be required to prepare financial statements that have not been prepared in specific prior periods, thereby putting a significant burden on the seller. For example, seller company A with historic audited financial statement prepared on a calendar year end basis, entered into a transaction that closed at September 30, was required to prepare audited financial statements at September 30 as well as internal statements on a TTM basis at March 31st of the current and prior year to meet the financial reporting requirements of the buyer faced. The challenge of creating interim statements that had not been prepared in the past and did not have account reconciliations that rolled forward and were cut off on this basis was significant.

I have seen more company accounting departments that are not staffed with the depth and breadth of staff to support an external audit and/or a company sale transactions than those that are, mainly because sell side transactions, as described above are not typically staffed for in many businesses. In cases where the accounting function of the seller is capable of supporting the external audit process, it often cannot support the due diligence requirements of a sales transaction due to demands and timeline of the due diligence process due to gaps in expertise and the day-to-day demands placed on the accounting function by the business. Simply put, many if not most of the private company accounting departments I have helped are not structured and staffed to handle sell side transactions. Outlined below is a generalized description of in house accounting department capability that I have worked with in medium to small companies in connection with support of external audits and sell side transactions:

1) The accounting function is limited to posting daily and month end transactions as part of a closing process using accounting software;

2)

the accounting function can perform step 1) and can also prepare account

reconciliations and internal financial statements;

3)

the accounting function can perform steps 1) and 2) as well as generate

prepared by client schedules (PBC's) for a year-end audit;

4)

the accounting function can perform steps 1), 2) and 3) as well as financial

statements (i.e. balance sheet, income statement, cash flow statement and

footnotes) that can be opined on by the external audit firm;

5)

the accounting function can perform steps 1), 2), 3) and 4) above as well as

support the due diligence process in a sell side transaction.

In scenario 1) above, the accounting function typically does not have the ability to get through an external audit. In scenario 2) the accounting department may or may not have the capability to complete an external audit and will typically need outside help to do so. In scenario 3) the accounting function may be able to complete the external audit in its entirety but may need outside assistance. In scenario 4) the accounting department can support the external audit but in most cases not the sell side due diligence requirements or timeline. In scenario 5) the company has a staff with the depth, breadth and resources to complete steps 1) through 3) and an external audit 4) as well as support the due diligence requirements in a sell side transaction that results in the sale of the business. I have found scenario 5) situations to be somewhat rare in small to medium companies due to the cost and expertise required to meet this benchmark.

In my role as an outside consultant and internal staff, I have been typically asked to work in scenarios 3), 4) and 5) with or in addition to the existing accounting department however I have also worked in scenario 1) and 2) situations in order to assist businesses get to the point in the process where it can prepare PBC's in support of an audit. The key here for the seller is to plan and invest ahead. I have worked with successful entrepreneurs who invested in their accounting function who had level 5) capability over multiple years which allowed them to produce reliable historic information and other information that has bolstered their credibility over the long-term which made them more attractive sellers to credible buyers resulting in higher exit multiples. In other words, they generated a large return on their investment on their accounting and finance function. I have also seen level 1) accounting function capability businesses that have had sales transactions stall, enterprise values lowered or transactions not be completed at all, due to financial reporting and/or internal control issues.

The manta here is that the returns on accounting department capability in a transaction is significant based on exit multiples. because of this, the case can be made for engaging outside accounting/transaction expertise when it does not exist in house. In more basic and stark terms, I have witnessed stalled and terminated sales transactions due to the lack of investment in the skill and expertise needed to complete audits and/or due diligence aspects of the transactions. Transactions that were successfully closed typically were sales of businesses that had been audited for at least three years with clean audit opinions that also had the ability to produce the documentation and information required by the due diligence process. I have worked on transactions that have both closed and failed to close.

In conclusion, the timeline and deliverables in a sell side transaction to complete an audit and sale transaction are significant in this day and age and create a material burden on the seller that they often cannot meet with internal resources. Timeline demands also typically create a significant amount of stress on the seller. Put another way, the deliverables and timeline are often beyond the existing accounting function capability of many medium and small sellers unless specifically planned for, staffed for and invested in. Furthermore, the investment is generally more expensive if deferred or if not made in prior years to the year a transaction close is undertaken. My recommendation here is to plan ahead.

Please contact me on LinkedIn or at greggecarlson@gmail.com if you have any questions.